Medical Loan Calculator

Your Surgery Details

Your Monthly Payment

Understanding Your Costs

Based on UK medical loan rates (2025):

- 750+ credit score: 5.9%-7.9% APR

- 650-749 credit score: 8.5%-11.9% APR

- 580-649 credit score: 12.5%-18.9% APR

When you need surgery but can’t afford it out of pocket, the question isn’t just can you get a loan-it’s how do you get one, and what are the real costs involved?

Private surgery in the UK can cost anywhere from £2,000 for a simple procedure like a hernia repair to over £15,000 for complex surgeries like spinal fusion or full facial reconstruction. NHS waiting lists are long, and many people turn to private providers for faster care. But paying upfront isn’t an option for most. That’s where medical loans come in.

How Medical Loans for Surgery Work

A medical loan is a personal loan specifically designed to cover healthcare expenses. Unlike credit cards, these loans offer fixed interest rates and set repayment terms-usually between 12 and 60 months. You apply directly with a lender, get approved based on your credit score and income, and then receive the funds to pay your surgeon or clinic directly.

Many private hospitals in the UK have partnered with finance companies like My Medical Loan is a UK-based medical financing provider offering loans for cosmetic and non-elective surgeries with terms up to 60 months, MediFinance is a lender specializing in private surgical procedures with flexible repayment options, and Health Finance UK is a provider offering interest-free periods for qualifying procedures. These companies handle the payment to the clinic, so you don’t have to pay the full amount upfront.

Some lenders even offer interest-free periods-often 6 to 12 months-if you pay off the balance within that window. That’s a big deal if you’re getting a procedure like a knee replacement or breast reduction and can manage payments after recovery.

What Types of Surgery Can You Finance?

You can get a loan for almost any private surgical procedure, whether it’s elective or medically necessary. Common examples include:

- Facelifts, rhinoplasty, breast augmentation (cosmetic)

- Spinal surgery, hip replacements, cataract removal (medically necessary)

- Liposuction, tummy tucks, gender-affirming surgery

- Dental implants, jaw realignment, skin cancer removal

Some lenders won’t cover purely cosmetic procedures unless they’re performed by a registered surgeon in a regulated clinic. Others will fund anything as long as the provider is approved. Always check the lender’s list of accepted clinics before applying.

Eligibility: Do You Qualify?

You don’t need perfect credit, but you do need a steady income. Most lenders require:

- A minimum credit score of 600 (fair credit)

- Proof of income-pay stubs, bank statements, or tax returns

- UK residency and a bank account

- Age 18 or older

If your credit score is below 600, you might still qualify with a co-signer or by putting down a larger deposit. Some lenders allow you to pay 10-20% upfront and finance the rest.

One common mistake people make is assuming they need excellent credit. That’s not true. A 2024 study by the UK Finance Association found that 43% of approved medical loans went to applicants with credit scores between 580 and 670. It’s not about being perfect-it’s about being consistent.

Interest Rates and Fees: What You’ll Actually Pay

Interest rates vary widely. Here’s what you’re likely to see in late 2025:

| Credit Score | Interest Rate Range | Example: £8,000 Loan Over 3 Years |

|---|---|---|

| 750+ | 5.9% - 7.9% | £245/month • Total interest: £780 |

| 650-749 | 8.5% - 11.9% | £258/month • Total interest: £1,300 |

| 580-649 | 12.5% - 18.9% | £278/month • Total interest: £2,000 |

Watch out for hidden fees. Some lenders charge arrangement fees (up to £200), late payment fees (£15-£30), or early repayment penalties. Always read the fine print. The best lenders list all fees upfront.

Alternatives to Medical Loans

Loans aren’t your only option. Here are three others:

- Payment plans directly through the clinic - Many private hospitals offer in-house financing with 0% interest for 6-12 months. No credit check needed. But if you miss a payment, the full balance can become due immediately.

- Credit cards with 0% intro APR - Useful for smaller procedures under £5,000. Just make sure you pay it off before the promotional period ends. Otherwise, rates jump to 20%+.

- Health savings accounts (HSAs) - If you have one, you can use pre-tax money to pay for qualified medical expenses. But HSAs are rare in the UK-most people use ISAs or general savings.

Many patients combine options: pay 20% upfront with savings, finance the rest. That lowers monthly payments and reduces interest over time.

What to Watch Out For

There are scams. Some companies promise “no credit check” loans but charge sky-high fees or don’t actually pay the surgeon. Always verify:

- The lender is registered with the Financial Conduct Authority (FCA)

- The clinic is registered with the Care Quality Commission (CQC)

- You’re signing a contract with clear repayment terms

If a lender pressures you to sign quickly or won’t send documents in writing, walk away. Legitimate lenders give you 14 days to cancel without penalty under UK law.

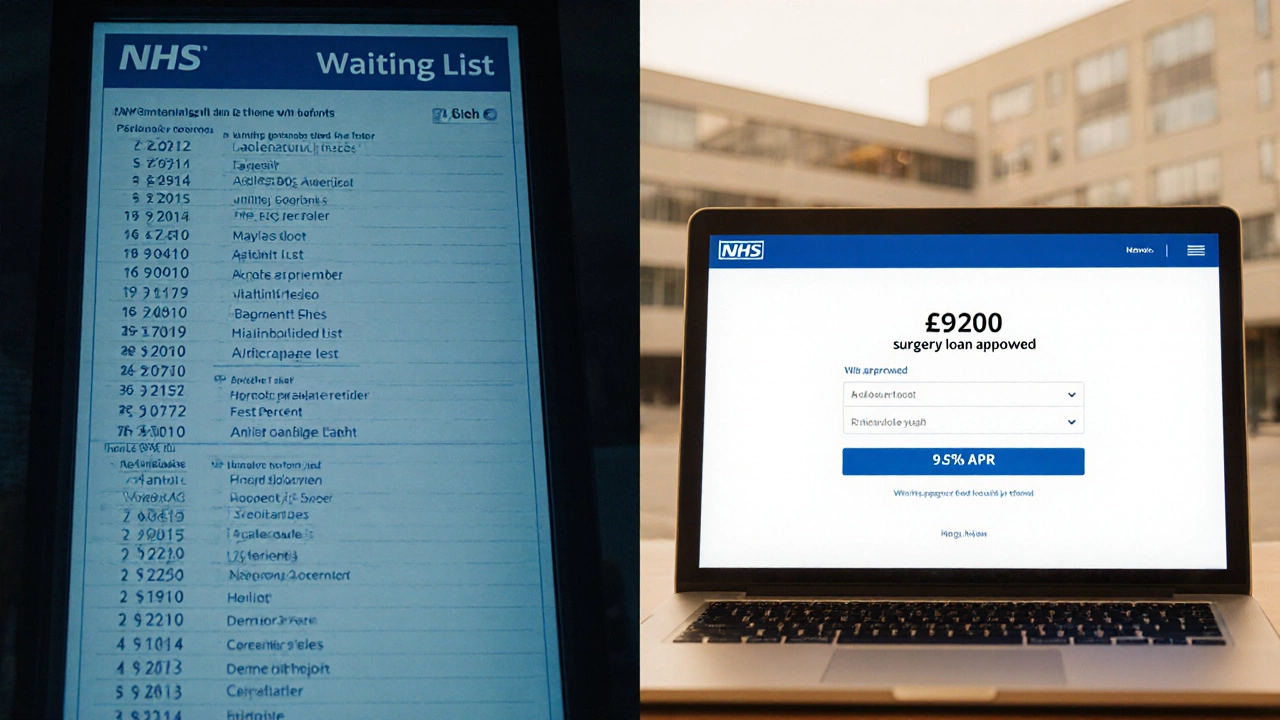

Real-Life Example: Sarah’s Knee Replacement

Sarah, 58, from Manchester, needed a total knee replacement. The NHS wait was 18 months. She found a private clinic offering the surgery for £9,200. She had £2,000 saved and applied for a medical loan for the rest.

She was approved for a 48-month loan at 9.5% APR. Her monthly payment: £220. She also got a 6-month interest-free grace period, which gave her time to recover before payments started. After 18 months, she paid off the remaining balance early and saved £410 in interest.

"It wasn’t easy, but I didn’t want to spend another year in pain," she said. "The loan made it possible-and the clinic handled everything with the lender. I never had to juggle bills."

Next Steps: How to Apply

If you’re ready to explore financing:

- Get a quote from your chosen clinic. Ask for a detailed breakdown of costs.

- Check your credit score (free via Experian or Equifax).

- Compare 3-5 lenders. Look at total cost, not just monthly payments.

- Apply with the best fit. Most approvals take 1-3 business days.

- Once approved, the lender pays the clinic directly. You start payments on your schedule.

Don’t wait until you’re in pain to start researching. The more time you have to compare options, the better deal you’ll get.

Can you get a loan for any type of surgery in the UK?

Yes, you can get a loan for almost any private surgical procedure, including cosmetic, reconstructive, and medically necessary surgeries. Most lenders cover everything from rhinoplasty to spinal fusion, as long as the clinic is registered and the surgeon is qualified. Some lenders have restrictions on purely aesthetic procedures, so always confirm with the lender first.

Do medical loans affect your credit score?

Applying for a loan triggers a hard credit check, which can temporarily lower your score by a few points. But making on-time payments over time will improve your credit. Missing payments or defaulting will hurt your score significantly. The key is consistency-treat it like any other loan.

Is it better to use a credit card or a medical loan for surgery?

For smaller procedures under £5,000, a 0% APR credit card might be cheaper if you pay it off before the intro period ends. For larger costs, a medical loan is almost always better. Loans have lower interest rates, fixed payments, and longer terms-making monthly payments more manageable. Credit cards can turn expensive fast if you only make minimum payments.

Can you get a loan if you’re self-employed?

Yes. Many lenders accept bank statements, tax returns, or SA302 forms from HMRC as proof of income. You may need to show at least 12-24 months of consistent earnings. Some lenders specialize in self-employed borrowers, so it’s worth shopping around.

What happens if you can’t make your loan payments?

Contact your lender immediately. Many offer hardship programs-temporary payment reductions, deferments, or extended terms. Ignoring payments leads to late fees, credit damage, and possibly legal action. But lenders prefer to work with you if you reach out early. Don’t wait until you’re behind.