PPO vs. HMO Cost & Flexibility Calculator

Your Profile

Recommendation

HMO Est. Annual Cost

$0

Lower Premium + ReferralsPPO Est. Annual Cost

$0

Higher Premium + FreedomEnter your details to see how PPO flexibility impacts your annual healthcare costs compared to an HMO.

Have you ever looked at your monthly health insurance bill and wondered why the number is so much higher than it used to be? If you have a Preferred Provider Organization (PPO) plan, that shock isn't just in your head. PPO plans are consistently among the most expensive types of health insurance available on the market. While they offer incredible freedom to choose doctors, that flexibility comes with a steep price tag.

You aren't paying for coverage alone; you are paying for the administrative machinery required to keep those doors open. To understand why your premium is what it is, we need to look under the hood of how these networks operate, who gets paid, and where the money actually goes.

Quick Summary: Why PPOs Cost More

- Larger Networks: PPOs contract with far more providers than HMOs, increasing administrative overhead.

- No Gatekeepers: You skip referrals, which saves time but removes cost-control mechanisms insurers rely on.

- Higher Negotiated Rates: Providers charge higher rates within PPO networks compared to restrictive HMO contracts.

- Out-of-Network Coverage: The ability to see any doctor anywhere adds significant risk and cost to the insurer's model.

- Administrative Bloat: Complex billing systems handle millions of claims from diverse providers.

The Freedom Tax: Understanding Network Size

The primary reason PPO insurance costs more lies in its defining feature: the size of its provider network. When an insurance company builds a PPO, they don't just pick a few local clinics. They negotiate contracts with thousands of hospitals, specialists, and independent practitioners across vast geographic areas. Sometimes this covers an entire state or even multiple states.

Maintaining these relationships is expensive. Every hospital needs a contract. Every specialist needs a rate agreement. The insurance company employs large teams of network managers whose sole job is to ensure these providers stay onboarded and compliant. In contrast, a Health Maintenance Organization (HMO) might only contract with a specific group of doctors in one city. The administrative burden of managing a PPO network is exponentially higher.

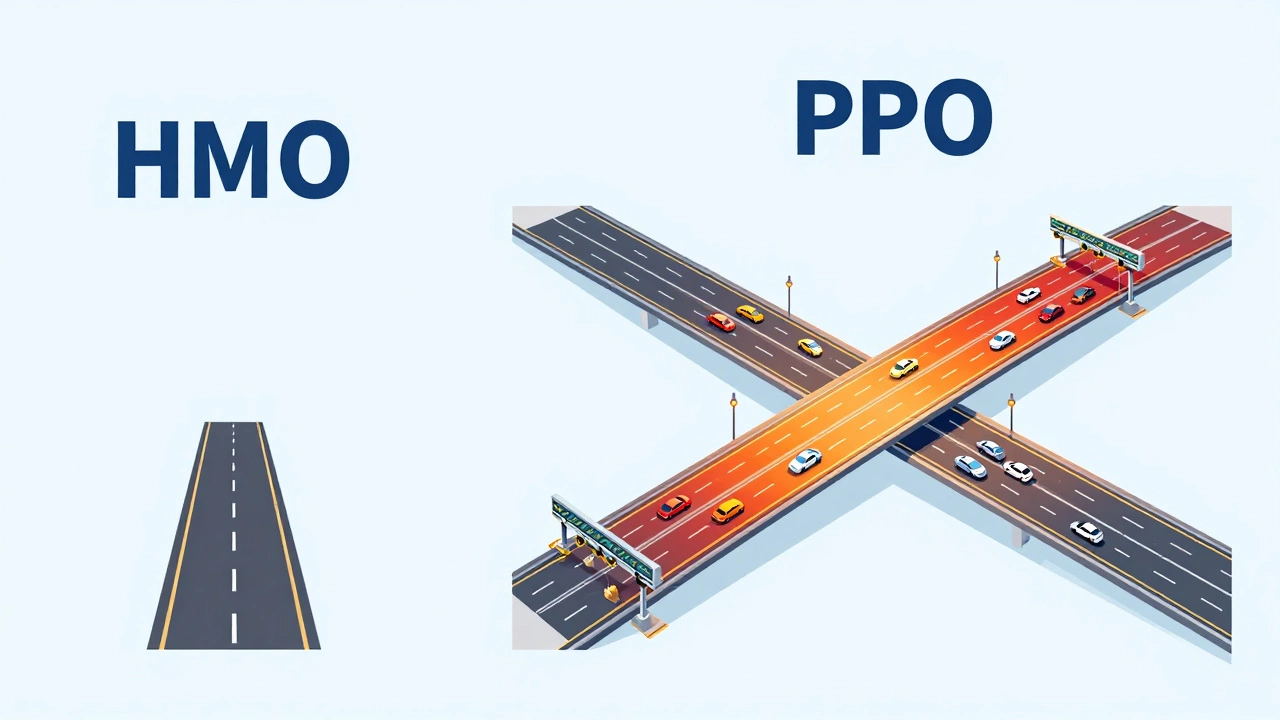

Think of it like building a road system. An HMO is a single-lane road connecting your house to work. It’s cheap to build and maintain. A PPO is an interstate highway system connecting every town in the country. The construction, maintenance, and toll collection costs are massive. You pay for that infrastructure through your premiums.

Skipping the Gatekeeper: The Referral Loophole

In many HMO plans, you must see a Primary Care Physician (PCP) first. This PCP acts as a "gatekeeper." If you have back pain, the PCP evaluates you. If they think you need an MRI, they refer you. If they think you need physical therapy, they send you there. This step controls costs because the PCP can often treat minor issues without expensive tests or specialist visits.

PPO plans remove this gatekeeper. You can walk straight to the orthopedic surgeon for that back pain. No referral needed. For you, this is convenience. For the insurance company, this is a financial risk. Without a PCP filtering out unnecessary visits, patients tend to utilize more expensive services. Specialists are paid significantly more per visit than general practitioners. When patients self-refer to specialists, the total cost of care rises sharply.

This lack of coordination leads to fragmented care. You might see three different specialists for related symptoms, each ordering their own set of blood tests. The insurer pays for all of them. In an HMO, the PCP would coordinate these tests, avoiding duplication. The efficiency savings in HMOs translate to lower premiums. The inefficiency in PPOs translates to higher bills for you.

Negotiating Power and Provider Rates

Insurance companies don't pay the full sticker price for medical services. They negotiate discounted rates with providers. However, the discount structure differs between plan types. Because PPOs allow patients to go out-of-network (though at a higher cost), providers within the network know they have leverage. They know patients value the choice.

Hospitals and large medical groups often demand higher reimbursement rates from PPO insurers than they do from HMO insurers. Why? Because PPO patients are less likely to switch doctors if prices rise slightly, whereas HMO patients are locked into a specific network. Providers play this dynamic against insurers during contract renewals. The result is that the base cost of care within a PPO network is often higher than within a tightly controlled HMO network.

Additionally, PPOs must cover "out-of-network" care. Even though you pay a larger share when you go outside the network, the insurer still has to process these claims and adhere to federal regulations regarding maximum out-of-pocket limits. This liability requires the insurer to hold more reserves, which drives up the baseline premium for everyone in the pool.

Administrative Overhead and Billing Complexity

Behind every claim is a mountain of paperwork. PPO plans generate a staggering volume of claims data. Because there is no central coordinator (like an HMO PCP), claims come in from hundreds of different sources. Each hospital uses different coding systems. Each specialist submits bills differently. The insurer needs sophisticated software and large staffs of claims adjusters to process this information accurately.

This administrative bloat is a significant driver of cost. Studies suggest that administrative expenses can account for 15% to 20% of total healthcare spending in the US. PPOs sit on the higher end of this spectrum. The complexity of balancing in-network versus out-of-network benefits, calculating co-insurance percentages, and applying deductibles requires robust IT infrastructure and human oversight. These costs are baked directly into your monthly premium.

| Factor | PPO Impact | HMO Impact |

|---|---|---|

| Network Size | Very Large (High Admin Cost) | Small/Medium (Low Admin Cost) |

| Referrals Required | No (Higher Utilization) | Yes (Controlled Utilization) |

| Out-of-Network Coverage | Yes (High Liability) | No (Except Emergencies) |

| Provider Negotiation Power | Lower (Providers Demand More) | Higher (Insurers Control Access) |

| Patient Flexibility | High | Low |

Risk Pooling and Adverse Selection

Insurance works by pooling risk. Healthy people pay premiums that help cover the sick people. However, PPO plans attract a specific type of enrollee. People who want PPOs are often those who already have established relationships with preferred specialists or who anticipate needing complex care. They are willing to pay extra for that access.

This creates a phenomenon called adverse selection. The risk pool for PPOs tends to be sicker or more utilization-heavy than the pool for HMOs, which often attracts younger, healthier individuals looking for the cheapest option. When the average member uses more care, the insurer must raise premiums to cover the payouts. It’s a cycle: higher costs lead to higher premiums, which drive away the healthiest members, leaving an even sicker pool behind.

Furthermore, because PPOs cover out-of-network care, they face unpredictable spikes in costs. If a member chooses an expensive out-of-network surgeon, the insurer absorbs part of that cost. These unpredictable losses must be hedged against by raising the standard premium for all members, regardless of whether they use out-of-network providers.

The Hidden Cost of Choice

Ultimately, the high cost of PPO insurance is the price of consumer sovereignty. You are buying the right to ignore restrictions. You are paying to avoid asking permission for a specialist visit. You are paying to keep your current doctor even if you move cities. While this feels valuable-and it is-it disrupts the cost-containment strategies that insurers use to keep premiums low.

If you never change doctors, rarely see specialists, and don't mind coordinating care through a primary physician, a PPO is likely overkill. But if you travel frequently, have chronic conditions requiring multiple specialists, or simply value the peace of mind that comes with unlimited choice, the higher premium may be worth it. Understanding these mechanics helps you decide if the freedom is truly worth the financial trade-off.

Frequently Asked Questions

Is a PPO always more expensive than an HMO?

In almost all cases, yes. PPO premiums are typically 20% to 40% higher than comparable HMO plans. This is due to the larger network size, lack of gatekeeping, and out-of-network coverage options. However, if you frequently use out-of-network providers, an HMO could effectively cost you more in denied claims, making the PPO the safer financial choice despite the higher premium.

Why do doctors prefer PPO plans?

Doctors often prefer PPOs because they face fewer administrative hurdles. They don't need prior authorizations for most procedures, and they can see patients without referrals. Additionally, PPO reimbursement rates are generally higher than HMO rates, allowing providers to earn more per visit. This preference reinforces the cycle of high costs, as providers lobby to stay in PPO networks.

Can I lower my PPO costs?

Yes, by choosing a High-Deductible Health Plan (HDHP) paired with a PPO. This lowers your monthly premium significantly. You pay more out-of-pocket before insurance kicks in, but you retain the network flexibility. Another strategy is to strictly use in-network providers. Going out-of-network drastically increases your share of the cost, negating the benefits of the PPO structure.

What happens if I go out-of-network with a PPO?

You will pay a higher percentage of the bill, known as coinsurance. For example, while you might pay 20% for in-network care, you could pay 40% or 50% for out-of-network care. Additionally, out-of-network costs usually count toward a separate, higher deductible. Be aware of "surprise billing," where balance billing occurs if the provider hasn't contracted with your insurer, though recent laws have limited this in emergency situations.

Do employers subsidize PPO costs?

Many employers do subsidize a portion of PPO premiums, but they often encourage employees to choose cheaper plans like HMOs or EPOs by offering higher subsidies for those options. Check your employer's benefit summary to see the "true cost" of your PPO. Sometimes the employee contribution is small, masking the actual high price of the plan.